Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs Replimune Group (NASDAQ:REPL) A Risky Investment?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Replimune Group, Inc. (NASDAQ:REPL) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

What Is Replimune Group's Debt?

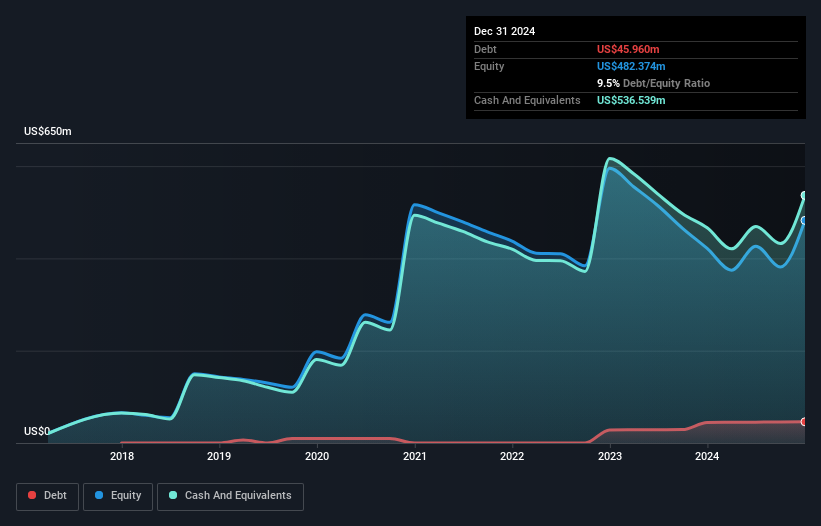

The chart below, which you can click on for greater detail, shows that Replimune Group had US$46.0m in debt in December 2024; about the same as the year before. However, its balance sheet shows it holds US$536.5m in cash, so it actually has US$490.6m net cash.

How Healthy Is Replimune Group's Balance Sheet?

The latest balance sheet data shows that Replimune Group had liabilities of US$47.9m due within a year, and liabilities of US$73.4m falling due after that. Offsetting this, it had US$536.5m in cash and US$3.07m in receivables that were due within 12 months. So it actually has US$418.4m more liquid assets than total liabilities.

This excess liquidity is a great indication that Replimune Group's balance sheet is almost as strong as Fort Knox. Having regard to this fact, we think its balance sheet is as strong as an ox. Succinctly put, Replimune Group boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Replimune Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts .

See our latest analysis for Replimune Group

Given its lack of meaningful operating revenue, Replimune Group shareholders no doubt hope it can fund itself until it has a profitable product.

So How Risky Is Replimune Group?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that Replimune Group had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$192m of cash and made a loss of US$228m. While this does make the company a bit risky, it's important to remember it has net cash of US$490.6m. That kitty means the company can keep spending for growth for at least two years, at current rates. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Replimune Group (1 is a bit concerning!) that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.