Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalSBM Offshore's (AMS:SBMO) Upcoming Dividend Will Be Larger Than Last Year's

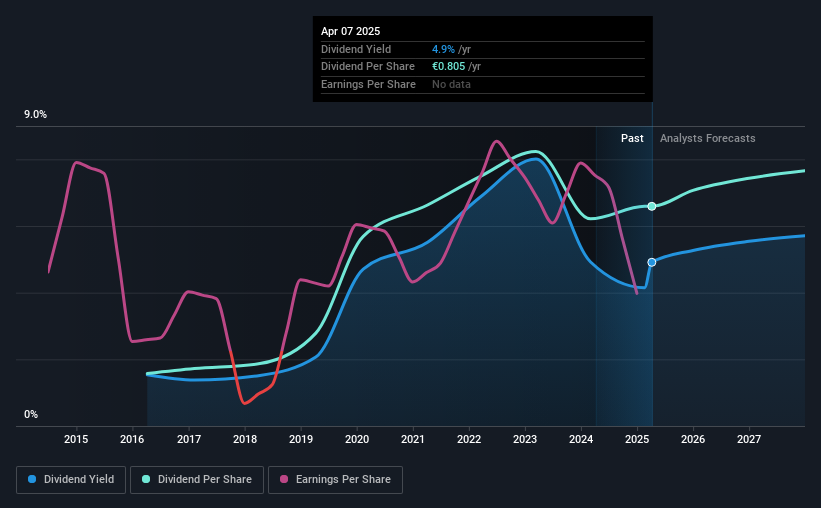

SBM Offshore N.V. (AMS:SBMO) has announced that it will be increasing its dividend from last year's comparable payment on the 6th of May to $0.851. This makes the dividend yield 4.9%, which is above the industry average.

SBM Offshore's Payment Could Potentially Have Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Prior to this announcement, the company was paying out 105% of what it was earning, however the dividend was quite comfortably covered by free cash flows at a cash payout ratio of only 11%. Healthy cash flows are always a positive sign, especially when they quite easily cover the dividend.

Looking forward, earnings per share is forecast to rise exponentially over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 21%, which would make us comfortable with the dividend's sustainability, despite the levels currently being elevated.

Check out our latest analysis for SBM Offshore

SBM Offshore's Dividend Has Lacked Consistency

SBM Offshore has been paying dividends for a while, but the track record isn't stellar. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. The annual payment during the last 9 years was $0.21 in 2016, and the most recent fiscal year payment was $0.88. This implies that the company grew its distributions at a yearly rate of about 17% over that duration. SBM Offshore has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Has Limited Growth Potential

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Earnings per share has been sinking by 14% over the last five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. On the bright side, earnings are predicted to gain some ground over the next year, but until this turns into a pattern we wouldn't be feeling too comfortable.

The Dividend Could Prove To Be Unreliable

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Just as an example, we've come across 3 warning signs for SBM Offshore you should be aware of, and 1 of them is significant. Is SBM Offshore not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.