Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalUndervalued Indian Stocks To Watch In September 2024

The Indian market has shown robust performance, rising 1.0% in the last 7 days and climbing 45% over the past year, with earnings expected to grow by 17% annually in the coming years. In this favorable environment, identifying undervalued stocks that have strong growth potential can be a strategic move for investors looking to capitalize on market opportunities.

Top 10 Undervalued Stocks Based On Cash Flows In India

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Everest Kanto Cylinder (NSEI:EKC) | ₹185.42 | ₹306.01 | 39.4% |

| Apollo Pipes (BSE:531761) | ₹605.20 | ₹1146.89 | 47.2% |

| Venus Pipes and Tubes (NSEI:VENUSPIPES) | ₹2429.90 | ₹4380.46 | 44.5% |

| Updater Services (NSEI:UDS) | ₹354.15 | ₹621.13 | 43% |

| IOL Chemicals and Pharmaceuticals (BSE:524164) | ₹441.00 | ₹762.32 | 42.2% |

| Vedanta (NSEI:VEDL) | ₹468.45 | ₹934.38 | 49.9% |

| Prataap Snacks (NSEI:DIAMONDYD) | ₹856.90 | ₹1509.79 | 43.2% |

| Patel Engineering (BSE:531120) | ₹57.24 | ₹92.46 | 38.1% |

| Rajesh Exports (NSEI:RAJESHEXPO) | ₹292.95 | ₹585.61 | 50% |

| Mahindra Logistics (NSEI:MAHLOG) | ₹498.10 | ₹994.06 | 49.9% |

Below we spotlight a couple of our favorites from our exclusive screener.

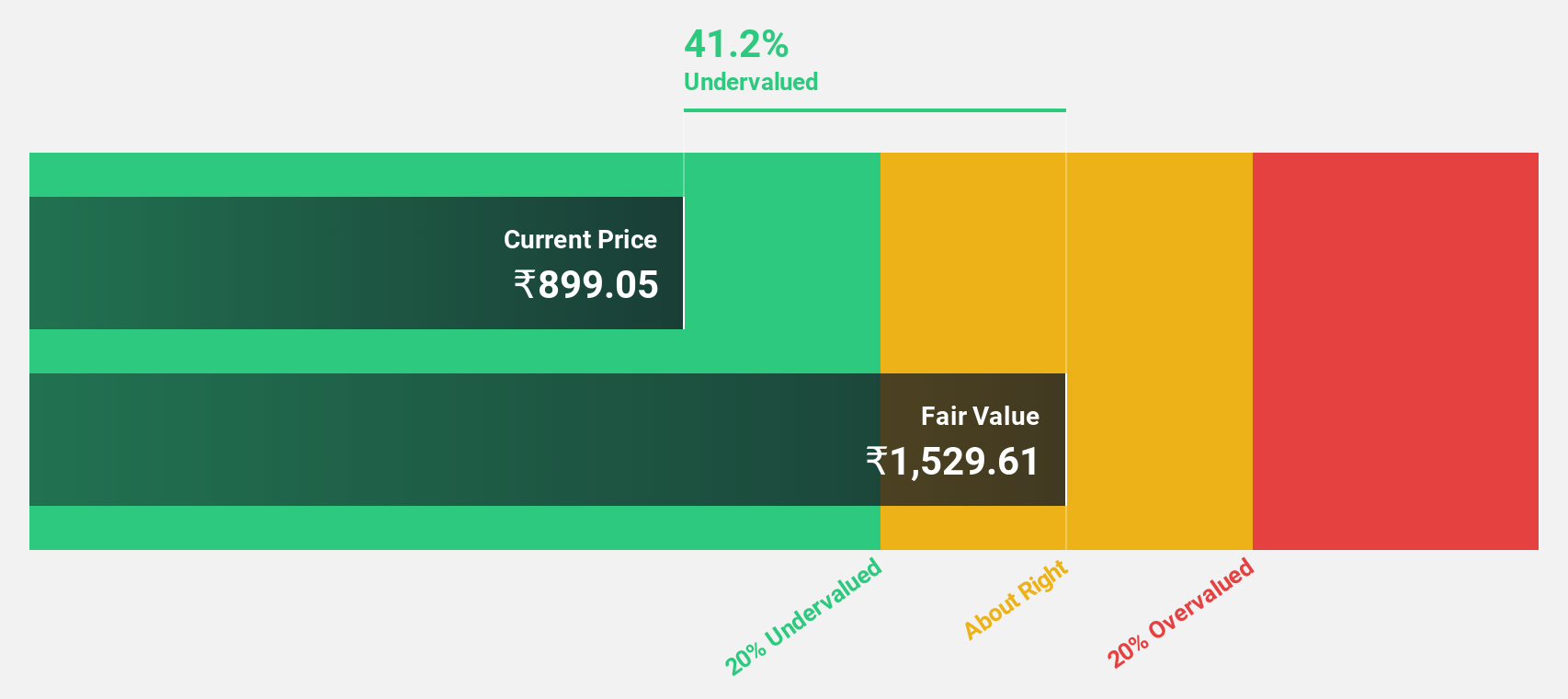

Jindal Steel & Power (NSEI:JINDALSTEL)

Overview: Jindal Steel & Power Limited operates in the steel, mining, and infrastructure sectors in India and internationally, with a market cap of ₹989.89 billion.

Operations: The company generates revenue primarily from manufacturing steel products, amounting to ₹510.56 billion.

Estimated Discount To Fair Value: 20.1%

Jindal Steel & Power (₹970.4) is trading at 20.1% below its estimated fair value of ₹1214.09, indicating it may be undervalued based on cash flows. Despite a recent dip in net income to ₹13,401.5 million for Q1 2024 from ₹16,869.4 million a year ago, the company’s earnings are forecasted to grow significantly at 24% annually over the next three years, outpacing the Indian market's projected growth rate of 17%.

- The analysis detailed in our Jindal Steel & Power growth report hints at robust future financial performance.

- Click here to discover the nuances of Jindal Steel & Power with our detailed financial health report.

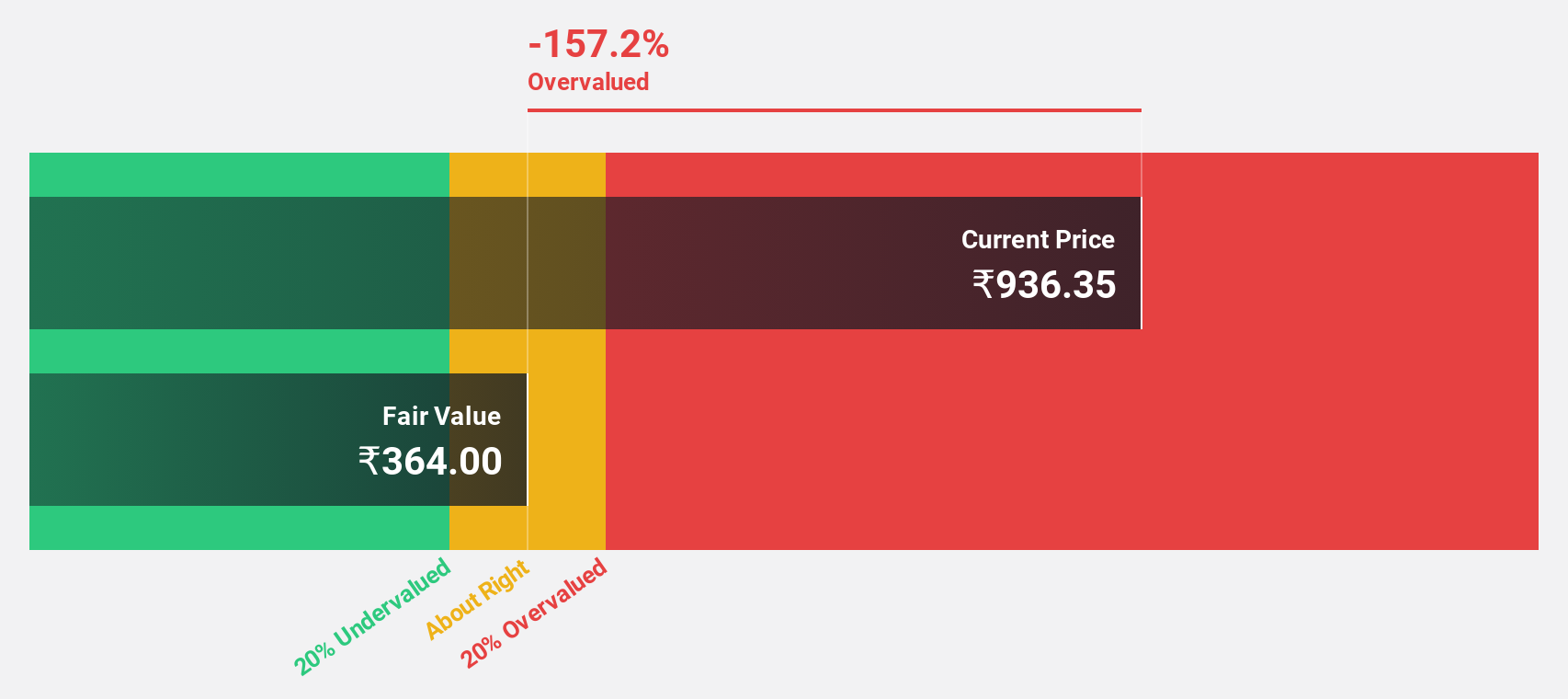

Titagarh Rail Systems (NSEI:TITAGARH)

Overview: Titagarh Rail Systems Limited manufactures and sells freight and passenger rail systems in India and internationally, with a market cap of ₹191.75 billion.

Operations: The company generates revenue from two main segments: Passenger Rail Systems, contributing ₹3.32 billion, and Freight Rail Systems (including Shipbuilding, Bridges, and Defence), contributing ₹35.14 billion.

Estimated Discount To Fair Value: 33.8%

Titagarh Rail Systems (₹1423.8) is trading at 33.8% below its estimated fair value of ₹2151.1, suggesting it is undervalued based on cash flows. The company reported Q1 2024 net income of ₹670.1 million and has forecasted earnings growth of 30.1% annually over the next three years, surpassing the Indian market's projected growth rate of 17%. Despite recent shareholder dilution and high share price volatility, Titagarh's revenue is expected to grow at a robust 25.7% per year.

- Our expertly prepared growth report on Titagarh Rail Systems implies its future financial outlook may be stronger than recent results.

- Click to explore a detailed breakdown of our findings in Titagarh Rail Systems' balance sheet health report.

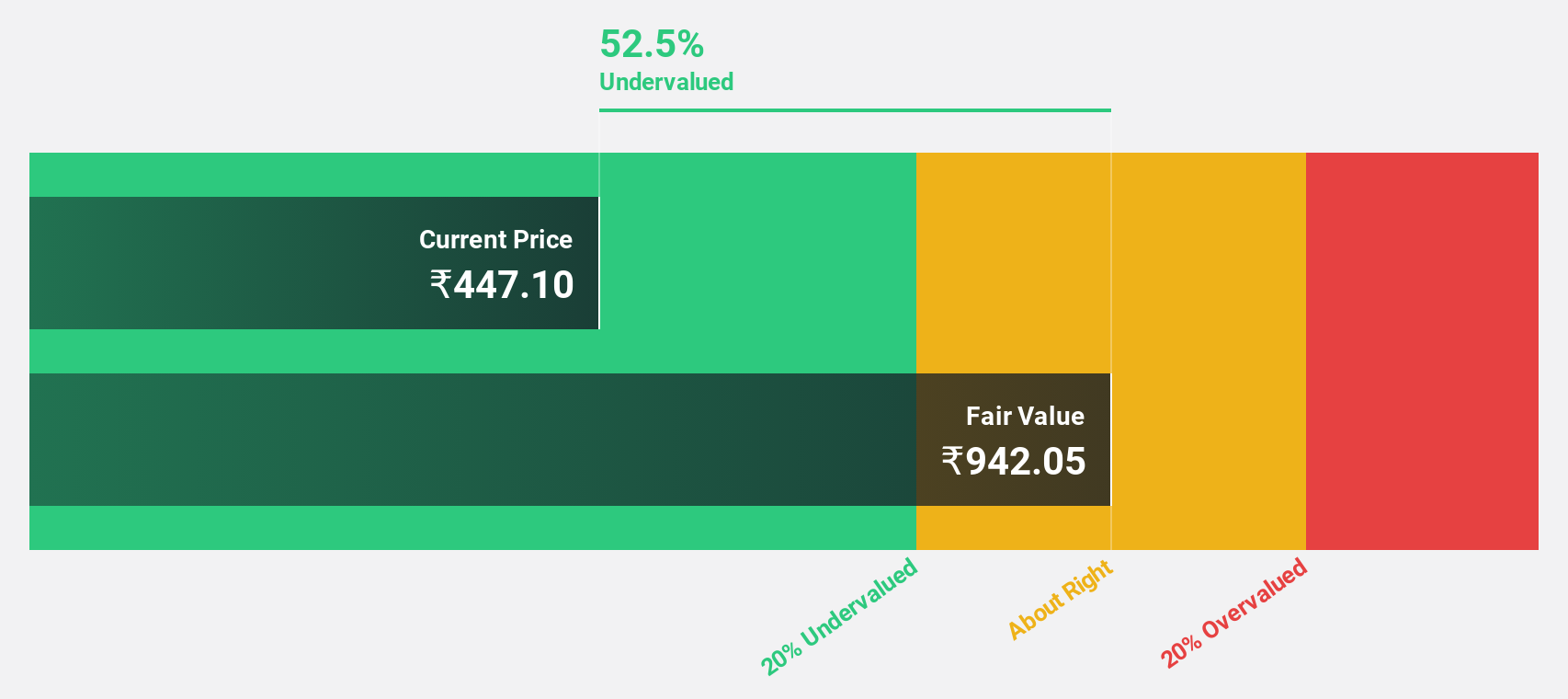

Vedanta (NSEI:VEDL)

Overview: Vedanta Limited, a diversified natural resources company with a market cap of ₹1.83 trillion, explores, extracts, and processes minerals and oil and gas in India and internationally.

Operations: Vedanta Limited generates revenue primarily from Aluminium (₹499.81 billion), Copper (₹197.31 billion), Oil and Gas (₹179.05 billion), Iron Ore (₹83.51 billion), Power (₹62.54 billion), and International Zinc operations (₹32.06 billion).

Estimated Discount To Fair Value: 49.9%

Vedanta Limited (₹468.45) is trading at 49.9% below its estimated fair value of ₹934.38, indicating significant undervaluation based on cash flows. The company's earnings are forecasted to grow significantly at 41.8% per year, outpacing the Indian market's growth rate of 17%. However, Vedanta has a high level of debt and profit margins have decreased from 6.2% to 3.6% over the past year, raising concerns about sustainability despite strong return on equity forecasts (47.2%).

- Our growth report here indicates Vedanta may be poised for an improving outlook.

- Take a closer look at Vedanta's balance sheet health here in our report.

Summing It All Up

- Gain an insight into the universe of 33 Undervalued Indian Stocks Based On Cash Flows by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

- PFF

- 30.17

- +0.13%